The Oak Bloke Q1 Performance Part Deux

The Oak Bloke Q1 Performance Part Deux

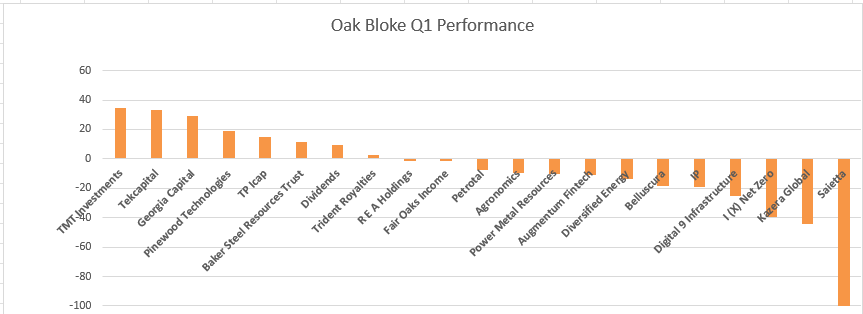

Now for the OB20 review

Dear reader

Let’s look at the OB 20:

I’m actually going to go worst to best.

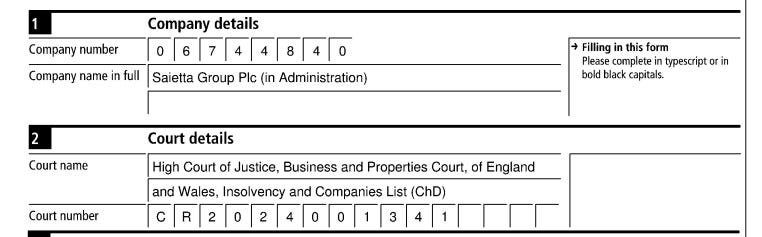

Saietta

A 100% loss. The albatross. Albatross! The lesson I take from this loss is to consider risk on a far more regular basis. To remove all trace of euphoria and put on the Black Hat of critical creative thinking. I wrote about the 6 hats of creative thinking last year.

Internet fora can provide plenty of Black Hat thinkers. I read a lot and even where I disagree I consider their line of thinking. Give it airtime in your head. Don’t be critical of the critical. Be as critical as the critical. Be pessimistic for a change.

Another lesson I could take was to exit once the odds were against me. Once the smart money were selling down their holdings. Once a notice to potentially be insolvent was given. Even 95% down you can salvage 5%. Better than 0%.

In my defence, I held hope that an 11th hour fund raise could be achieved. But it was not to be. I will pick over the bones once the Insolvency Practitioner releases their report. Maybe some further learnings can emerge.

I note that Saietta VNA in India appears to be “business as usual”.

Kazera

Down 44% YTD.

That sounds dreadful doesn’t it? But it’s down on zero news (and zero includes any news of the Hebei Construction paying the rest of the money owed for the purchase of the Aftan holding). But is the hold up a negative really? Interest accrues on the balance at 8% and multiple options still exist for KZG to factor (sell) the debt, or to sell the asset to another party, and keep the monies from Hebei. While Lithium is at a very low price, Tantalum isn’t, and the economics are attractive as a result.

KZG’s next door neighbour at that asset, Arcadia gives us important clues too. Their land surrounds Aftan, and is a further lithium/tantalum holding.

They tell us in their Interims:

“Hebei is to construct a plant, the necessary infrastructure and conduct the works to execute mine development and the commissioning of a Multi Gravity Separation plant (MGS). The funding of the construction is to be for a minimum value of US $7 million dollars.

Construction continued to progress during the half year with progress focused on road construction and the finalisation of design work for the water pipeline, power supply line, civil works for the plant and the procurement of processing equipment. Most of the processing equipment, including all long lead items, have already been ordered and are expected to arrive on site from April 2024, with longer lead items such as the spiral circuit and MGS expected to arrive from June 2024.”

This plant will be used to process Aftan.

Another reason for the drop was delays to production due to finding Monazite in the Heavy Mineral Sands and government radiological rules, but that gets fixed this month and the plant is ready to go and stockpiles of feed are ready to process.

I averaged down at 0.36p to take full advantage of this lull, this mispricing.

The mispricing of buying a £3.75m mar cap which has £8m of (growing) current assets and zero liabilities - let alone the 2 sets of plant and 2 mining operations which come online in April/May this year, according to this week’s interim results. I’ve written extensively as to the rationale and nothing has changed. I remain very bullish about KZG’s prospects.

As much as I spoke in my prior article of my lack of above £100m market caps, I do believe this one could gallop in a way a £100m company simply could not. The upside to a nano cap can be enormous if you can understand and control for risk and win more times than you lose and win bigger (i.e. more that double bag) than you lose (a lose is always a single bag)

I(X)

Again down 40% but on no news but with numerous upsides and a track record of rather too silently pulling rabbits out of hats. The sale to Occidental at 7.2X being an example, the upround to BP Ventures being another. I wrote about these a few days ago so don’t have much else to add - but read it and decide for yourself.

DGI9

I’ve just written an article covering the gains at DGI9 so again yes it’s down 25% YTD but dropped this year on the risk of Verne not completing, which is no longer a risk. So at the very least should rerate 33% but based on the increased valuations, earnings and prospects/outlook I believe the 75% discount is a nonsense.

IP Group

Again covered recently in IP Group Results Part 1 and Part 2. Down 19% YTD. There have been interesting debates over whether the management are too laid back, is this another “Wellcome Group”, and whether you should wait for definitive proof before investing, rather than buy and hold in anticipation of news. IPO’s holding on Oxford Nanopore (ONT) and ONT’s price drop YTD is the main reason for the 19% YTD fall. I am optimistic for ONT (as are IPO’s management) and for the many Phase 2/3 read outs coming. The fact that Biotech is a hot area as patent cliffs drive acquisitions from the majors.

Optimistic on its deeptech and greentech too. Will Fusion never happen? But what if it does? Even if it doesn’t a technology that furthers the cause towards can nevertheless prosper. Arguably the world need for Fusion to succeed to achieve long-term net zero. To meet the hunger for more and more energy.

I see SMT (Scottish Mortgage) is powering again. How long will it be until someone looks at the relative value at IPO and trades the difference? Compared to much of US Tech, this BritTech (and OzTech) is seriously cheap.

Belluscura

Down 18.5% YTD again on no news other than the fundraise which eluded Saietta didn’t elude BELL. Even Paul Scott in his recent podcast appeared to say this might be a good buy - he qualified that by saying he didn't know.

It is annoying that there is a lack of newsflow, but the completion of the merger with TMTA means the stars are aligned. My production, finance, sales, cash models based on the contract order book all appear to show this will re-rate during FY24.

DEC

Down 13.8%. I have added a lot of analyis to my bumper length DEC-iding a new course. I would encourage DEC-hands, prospective DEC-hands and even ex DEC-hands who jumped ship to consider what I’ve written. In the final day of this quarter DEC rose 6.2%

Yes, the dividend was cut by 2/3. Yes, that was seriously annoyed and unsettled people. Yes, you can certainly argue that Dusty appeared to give certain assurances. But. But. Considering this as a share I’ve never invested in and consider whether should I invest in it (that’s another technique I’m always VERY keen to employ). i.e. Remove the emotional baggage. Remove the history. Look at it objectively.

Profit up. Production up. Cost down. Environmental allegations - hugely solved. ARO - under control. Well retirement - under control. Nascent well plugging business making a tidy profit and capable of growing and making more. Tick. Post period another clever acquisition at an attractive multiple with zero baggage, and tapping into LNG premium prices. Some see Oaktree’s sale as a negative but DEC had 1st refusal. Choosing between a bigger dividend and a weaker balance sheet and a smaller div and stronger balance sheet and an accretive acquisition I’m glad Rusty did this. Much as I’d have loved to continue to receive a higher yield.

Risk. What risk remains? Do the shorters have a case? Why are the shorts growing? There’s certainly been a wall of negative UK momentum and some additional shorts perhaps rationalising the logic of taking advantage of a wall of negative UK sentiment as disaffected DEC-hands exit - but that’s a short short window. Soon the Q1 numbers will be out and we’ll see another strong showing. Each evening the US buys what the UK sells too.

If I’m right about what I’ve read (and written) about US natural gas supply and demand I believe the $1.66/mmbtu prices where no one makes money will be a distant memory in time. After $10 per BOE is a ridiculous price for natural gas. No one can make money - and DEC’s competitors are cutting production. The supply imbalance may clear in 2024 or 2025. I’m happy to wait. DEC is another holding whether topping up this year was a no brainer especially as I was lucky to catch slightly above the $8.50 YTD lows at $8.61.

AUGM

I also recently wrote about Augmentum Fintech in my article MMMillions. Down 11% YTD yet has only offered good news to the market.

If you’ve been watching the news this week about the Francis Scott Key bridge in Baltimore (and maybe like me caught the interview with the chap of Lloyds of London on Bloomberg) this made me think of Artificial one of AUGM’s holdings and I’d really encourage you to read about Artificial at the above link. I believe the sort of FinTech’s AUGM have can be game changers and game changers equal YTD rises not falls.

POW

Power Metals again has been a slew of good news, although tempered by a limited fund raise and a distinct change in direction towards Saudi Arabia - both for projects but also for funding. A 20:1 consolidation bizarrely dropped the price to YTD lows, so taking advantage of that again I averaged down at the opportunity. I believe the prospects of its holding in GMET and FCM are also very exciting, but have chosen to focus my holding in POW rather than buy all three. The Pilot Mountain opportunity with tungsten and garnet particularly caught my eye, as well as the Uranium IPO (UEE). Down 10% is just an opportunity as far as I’m concerned.

ANIC

Agronomics down 9.5% YTD. Well during Q1 this was up 40% and has dropped back on - you guessed it - no news. To my mind, even if only for the Blue Fin Tuna I believe this will do well. At $500/Kilo (and rising) Blue Fin Tuna is critically endangered yet people will eat it - with relish. (A teriyaki relish probably). Supply cannot meet demand for Tuna, actually. Cruelty-free leather. Again high-end fashion will embrace the ESG message and this will flourish.

But the reality is one of its holdings is commercialising Chicken. Chicken you can buy for what £5/kilo if you buy Tesco Value Chicken, they reckon they can produce competitively (although probably for more than £5). So how much money are the Blue Fin Tuna guys going to make if you can competitively make chicken via precision agriculture?

So how much money are the Blue Fin Tuna guys going to make if you can competitively make chicken?

Even today I was listening to Radio 4 and how farmers fields were flooded for the past 6 months. To how Cocoa is above $10k a tonne and our Easter Eggs are going to be less chocolately. Yes, ANIC have a Cocoa bean holding, and they are commercialising precision agriculture cocoa in Japan made via cellular agriculture. ANIC could be huge and it has bets on a wide range of possibilities in this sector - and have a track record - a growing NAV. A 40% discount for a growing NAV appears to offer clear value.

Petrotal

How this is at a loss YTD leaves me at a loss.

Apart from a positive Q4 update with growing production, a generous dividend, buy backs, there hasn’t been much news flow. But oil is up YTD, so a 7.8% fall at PTAL is strange.

A 3.33% dividend YTD and buy backs mean this is trundling away nicely for me.

Fair Oaks

YTD -1.4%. FAIR was meant as an income play so YTD gains wasn’t its reason to be included. It has had a YTD rise though but dropped back. The buy backs based on a discount, flipped to FAIR re-issuing the bought back shares from Treasury when its discount to NAV turned to a premium to NAV. I love that. Make money at both ends. The FAIR management team are smart, fair play to them!

There’s a 3.6% gain waiting in April from the Q1 dividend and my recent article FAIR dinkum covered why I think FAIR is undervalued relative to what the “official” NAV shows. I also noted Bloomberg reporting (on the TV) that the outlook for private credit defaults are extremely low. Yet FAIR are buying CLO equity at levels that assume serious amounts of loss. Hidden value.

R.E.A.

YTD -1.3%. This went ex-dividend on the last trading day of March. YTD was +15% until then. Why? Well the 11.5p a share dividend is worth 14.4% to OB followers who bought in at the start of the year. (i.e. at 80p). Why? Well 11.5/0.8 = 14.4. The 80p is effectively a 20p discount to the preference share issue price of £1. So 11.5p per £1 share which you could have bought for 80p.

I’ve certainly learnt a lesson around Preference Shares this year and I have CaneToad on the LSE RGL board to thank for that. At ESE (covered yesterday), at Regional REIT, and the RE.B I have to thank.

A great book I read was Joel Greenblatt’s “You can be a Stock Market Genius”. But I was frustrated that Warrants and Options are not usually available to us private investors (in the UK anyway).

Prefs seem to be a way to follow Joel’s advice.

I do need to write an article about REA - I’ve been remiss on that (well it’s been sat as a draft for several weeks). One of my readers, Damien, alerted me to REA today. He’s right in my view. The sale of a 35% share of one of its fields completed and the 90% discount to NAV offers serious upside and the FY2024 dividend offers an astonishing yield. More on that soon, reader.

We finally reach profit YTD, reader!

Trident

YTD up 2.7%.

Well, I think the market has completely missed the Oak Bloke’s musings on Trident.

Gold at $2,232, and a huge chunk of TRR’s producing portfolio is gold and many of its gold holdings are expanding production as I reported in my article TRR-ific - and we will see that in FY24 and FY25.

Meanwhile the Lithium price has bottomed, and is increasing. TRR’s share price has been punished for its Lithium holdings even though its Lithium royalties do not produce any Lithium yet! TRR has been punished for what it didn’t do, it’s like Derek Bentley, guilty by association for speaking about something it shouldn’t. Don’t let ‘em have it Chris.

Meanwhile many gold miners have shot up on higher gold and silver prices. As I result I sold gold holdings like HOC and bought more TRR because of this disconnect

Dividends!

9.5% YTD

Eagle-eyed readers will see I’ve sneaked in a “21st” holding. Rather than incorporate dividends to the 20 (19), I’ve decided to create another column. I’m anticipating between DEC, REA, PTAL, FAIR and TCAP to generate a 3.5% return (average across all 20) in 2024 even though only 1/4 of the OB holdings generate dividends. It would have been 5.5% if DEC had stuck to its 30% yield dividends!

For a portfolio which contains lots of growth potential (in my opinion), 5.5% would have been seriously impressive! But 3.5% isn’t bad! (especially as I argue DEC can invest in growth as a result).

BSRT

Up 11.4% YTD

This surprises me as it’s up 33% from its lows from November. This is another holding where news is sporadic. But when I read about its metallurgical coal “if only it could be funded” (but then was) I felt there was seriously overlooked value. I was right.

There is gold, gold royalties, there is Australian coal, there is Moroccan cement, plus other holdings. The Coal and Cement alone make this holding. The earnings and dividends we should see from FY25 should be substantial.

What interests me also is whether some of its bombed out holdings get support from BSRT using the cash flows rather than dividends (at attractive and accretive terms of course).

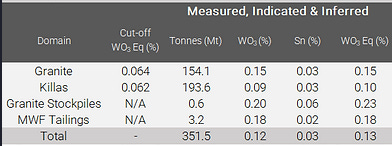

For example it’s not lost on me for all the “excitement” at GMET and regarding Tungsten at Pilot Mountain (in the USA), on the doorstep of its closest ally lies a large Tungsten deposit at a silly price.

Pilot Mountain has 12.53Mt at 0.27% W03 with significant copper-silver-zinc credits.

While Tungsten West has 315.5Mt at 0.12% W03 with tin credits.

TP ICAP

Up 14.6% YTD

A great year end update and mooting the minority sale of Parameta is a genius move. Holding on to Parameta is definitely the right decision. Expert after expert spoke to how selling it off would raise money. I exclaimed but you don’t understand their strategy! TP ICAP through a minority sale have found a genius middle way. They get to keep it but they get to part sell it.

I mused whether TP ICAP should have risen as much as CMC markets (Paul Scott’s top idea). There’s 9 month’s left for that.

Pinewood

It felt predictable that this was going to emerge at a profit, so a 18.8% YTD gain before it really has got started reflects the value here.

I look forward to seeing the progress here as it expands in the US as well as into Car Dealers. In my professional life I have been working with a chain of car dealers recently. I was gob smacked to see they were working with technology from the 1990s and running completely obsolete programs and applications. Pinewood is knocking on a door which desperately needs Pinewood’s software platform and capabilities.

Georgia Capital

CGEO remains on a huge discount and BGEO (Bank of Georgia) is on a tear. Even though this is up 29.3% YTD I am looking at the discount and at the growth and there’s more in the tank.

TEK

Tek was up 150% and now “only” up 33.3% YTD. It successfully floated SALT its Microsalt holding, and there is a string of positive news. It has raised funds this year (which caused the drop in the YTD), and that will fund Guident, working capital as well as a 6th holding linked to AI. Lucy released good and bad progress in Q4. We’ve spoken about BELL (TEK holds ~7% of BELL). Even for Lucy the emphasis now is on whether going from hundreds to thousands of stores can scale and grow profitability.

Between newsflow from its existing 5 holdings and its new 6th holding I believe TEK will flourish in 2024.

TMT

The 34.6% YTD gain is actually below my expectations. The IPO of Bolt will probably occur in 2025 which is a pity because on a mark-to-market basis Bolt compared to its close peers Uber and Lyft should probably be worth more than it currently is. It’s 2nd largest holding Backblaze has demonstrated enormous progress too.

A slew of gains as well as a robust culling of weak holdings made the FY23 results feel very forthright and solid, and I look forward to newsflow in FY24.

Well, reader, there’s the 20. I hope my musings have been useful as you make your own investment decisions.

As ever, this is not advice

Oak