136th article - an Oak Bloke Top 20 update

The pups are growing!

Dear Reader

Happy weekend and the sun is shining. The OB Top 20 stands at £19,741. A 1.3% loss YTD so for the eagle-eyed among you that’s a 1.2% improvement since my article 120 winners. For a change, I will not mention methane today.

Meanwhile Investor Chronicler Simon Thompson released his bargain shares 2024 yesterday. His list according to an internet forum is as below. I thought it would be interesting to track his tips against mine during 2024. I’m not a subscriber to IC (any more) so Simon won’t tell me why he backs these 8 without paying. I’ve “bought” an imaginary £1,000 of each share yesterday, with a £4 commission and used the buy price to determine the initial gain loss. (so same rules as OB Top 20). A 2.2% loss YTD.

So I’ll just give my initial and off the cuff thoughts on these 8, I considered ARTL for the OB Top 20 and concluded no thanks, with a large spread, a sub 3% yield, and a discount of “only” 40% I considered other discounts, spreads and yields more attractive. Poor ST starts with a 7% penalty on that one (or zero depending on how he measures it).

Moving to TENT, ST seems to have the same idea as the OB. Again I considered this for the Top 20 but while it was tempting I felt better opportunities lay elsewhere, for example with FAIR. I think TENT is pretty nailed on to do well, especially as it’s fallen about 15% since I considered it for the OB20.

Eenergy I recently looked at in a possible Arqiva vs SMS vs EEAS top trumps and concluded its foray into smart meters was very limited, but thought it was expensive for a small(ish) installation business subject to the whims of gov’t subsidies and regulation. CG and ED both see a doubling of profits in 2024 and a target price 60%-80% above the buy price so maybe there’s some upside. But compared to say the strategic informatics being delivered at far higher scale by Arqiva (held by DGI9) there’s really no comparison.

BP Marsh I do really like although again just a 20% discount to NAV, and the share price has doubled in price, my question would be how much upside can be expected? Pay an IC subscription to know more!

Anexo I know ST has been a fan of over a number of years. I read the recent update and noted the Accounts Receivable remains stubbornly high. Considering they said their focus was to slow down and generate cash they didn’t do a particularly good job! But the housing division is doing well (albeit is still small) and the legal cases are an upside “not in the price” (albeit the VW outcome of £7.7m disappointed most people - combined with the lack of transparency or should I say confidentiality of the win). It might do ok but I’d be surprised if it surprised (to the upside obviously).

I have no comment over the others but I may examine them at some point.

Deflection over - time for the OB 20 update

Well, do I start with my successes or losses? Losses obviously.

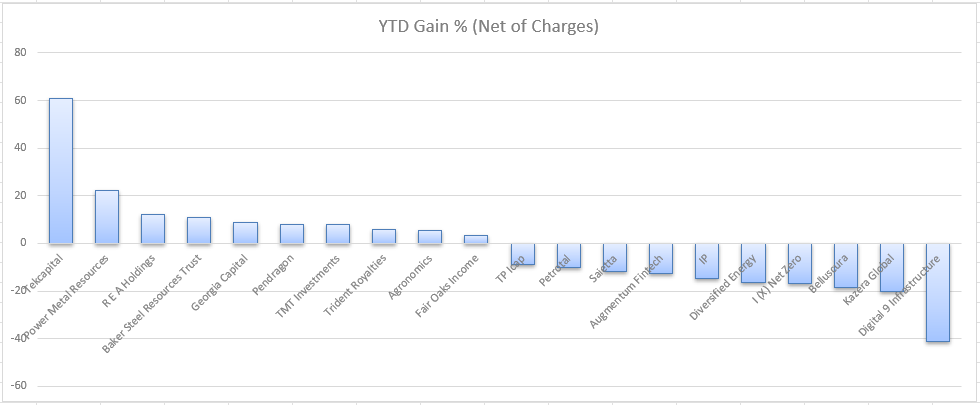

DGI9 down 40% YTD

A Market Cap now just £152m (and nadired at £120m during the week) for net assets of some £850m. Talk about cheap! This has plummeted on a few items of negative news.

First, another eruption slightly closer to the Iceland data centre (but still not close). The red dot is the data centre and the grey pin is the new eruption, and the little town further south is the prior eruption. The Ardian deal doesn’t cover volcanic eruption insurance so there’s maybe FUD which to my mind remains a very small risk for now. Bear in mind the Icelanders uses dykes to channel lava flows and can you spot a key asset next to Verne? (this airport serves the capital). I’m sure there’ll be Icelanders galore channeling lava away from Verne due to its location by the airport.

Second news of a regulatory delay in Iceland of +35 days while they look at Ardian more closely. So the deal might occur in mid Q2 not Q1. Hardly a reason for panic.

But what’s the risk if Iceland blocks the deal? Well this asset could be constrained by a lack of cash and crimp its growth, but no disaster.

The Triple Point Investment Manager in an interview in 2023 spoke to Verne generating £20m (0.4X the dividend) from “presold capacity” so is the “cash hungry” assumption actually just an assumption? What if the assetco can raise debt in its own right? (OB: Boom! 15/02/24 - today Verne raised $17m to fund expansion)

What’s the risk of DGI9’s debt itself? It’s true the RCF is costing DGI9 a fair bit of interest. Is there risk of DGI9 drowning in debt? Or not refinancing? For the detractors I’m sorry to say DGI9 have a covenant they are able to meet, and the facility has over 2 years of life remaining, so not a reason for undue panic in 2024.

I remain optimistic about the intrinsic value here although do I know this will come good specifically in 2024? (In time for judging the OB 20 on a 12 month basis). No, this negative sentiment and news flow may take time. The Verne delay doesn’t help in the very short term. DGI9 might end up be a longer-term play over a few years. So I may need to resign myself to this one (of the 20) being a potential drag for 2024.

In my own portfolio however (where a number of years is always my horizon) I’ve topped up DGI9 at these low prices - it was too tempting. The idea that a fire sale is “inevitable” is questionable.

Verne didn’t get sold at an 80% discount. It was at 25% if you believe the earn in is total garbage or slightly above book if you don’t. Either way that’s not an 85% discount is it? This idea that the TP management are a doom for DGI9, despite the assets being good I think is fanciful and not based on any facts. It’s true they messed up on their assumptions and expanded expecting to raise more and more equity but once that dried up they got caught short. Then interest rates shot up and vast outflows have occurred. The environment changed. Triple Point had a triple point whammy and DGI9 have paid the price. But I maintain, beyond the noise and panic there’s value in DGI9 beyond today’s share price. The many opinions of “No more than 30p” I find amusing. Based on what exactly?

Have the tailwinds behind demand for infrastructure which supports the growing use of the Internet changed? Not one iota!

KZG 20% down YTD

This is down on no news and we should see a number of key announcements in Q1. The next door neighbour Arcadians confirm Hebei is continuing to invest. KZG is poised for success with Diamond mining beginning this month and HMS beginning this quarter. I have no concerns here.

BELL 18% down YTD

Positive news where the £4.7m cash from the TMTA yawnfest has now flowed to BELL and my models point to a cash generative progress where it has a large bank of orders and clearly capability to grow that bank many times over, along with substantial improvements on costs to drive a higher margin. Yes, it is frustrating to not have real time visibility over sales and production but that’s normal in any share and the last trading update which says product launch early Feb 24 and full commercial launch March 24, with cash secured is now moving ahead at full speed.

I keep coming back to the simple fact there are Distributors who will ONLY sell BELL. Here are their US distributors:

IX down 17% YTD

Again on no news. Meanwhile yesterday ethanol-powered Ane Maersk began its first commercial journey powered by green methanol, and is “diligently searching” for new sources of methanol. With the Houthi’s disrupting the Red Sea the demand for shipping fuels is yet larger. Step in IX’s largest holding WasteFuel backed by Mr Buffett, Mr Maersk, BP and many more.

DEC down 16% YTD

After several weeks of silence, analyst after analyst this week have spoken out against the Snowcapped Nemeses, dismissing the slanted and inaccurate nature of the claims of their short report (i.e. short on facts, long on tales) and how in fact DEC continues to perform well and is forecast to continue (but you heard it first from the Oak Bloke). While the share price hasn’t leapt to reflect this yet, we draw closer to the ex-dividend date (the unaffected dividend mind you that DEC allegedly couldn’t afford). M&G are possibly still selling to cover their outflows. It’s their loss - quite literally.

Watching the coverage of DEC presenting to the West Virginia State Senators this week was interesting. A very different dynamic emerges about the perspective of the Republican controlled WV state government. The presenter from DEC is careful and polite to not criticise the federal regulators although the State Senators clearly believe the Feds haven’t a clue. It would be fascinating if DEC get to present similarly to Honorable Pallone and his committee as I believe the presentation was exemplory. DEC-hands can take a great deal of pride for the leadership DEC is exhibiting in the areas of methane testing, and in intelligently retiring wells once it is appropriate to do so. The hydrogen, geothermal, carbon capture and other programs they are working with organisations on was a good illustration why anti-DEC obsesssors like Cap’n Bleed refuse to even consider (which says something about their motives).

Peak Oil (and gas) isn’t a concept I’ve written much about but a fascinating podcast from GoRozen suggests the plentiful supply of gas may soon not be so plentiful and particularly not in the long run. What does that mean for prices? I posited that the Biden pause on LNG exports suggests someone knows something. The “hypermiling” DEC can do extremely well in an environment where “stewarding assets efficiently” is the KPI. Scarcity will quickly boost the price. It’s dangerous to be complacent about today’s price for natural gas being THE price.

While we wait, the hedges are proving to be a genius and defensive move.

Other “losers”

I’ve written about positive outlooks for IPO and AUGM this week so quite how they are at a loss leaves me at a loss. PTAL and TCAP on a loss are baffling too.

SED down 11% YTD

SED begins production this month and from Snowmobiles to see Northern Lights, to PGA product of the year award-winning Golf Mobiles SED is doing well outside India, and remains ready for a re-rating on stronger news.

The WINNERS!

TEK up 60% YTD

Microsalt (SALT)’s launch has been an unparelleled success for the UK and for TEK. Up 50% since launch.

Listening to SALT’s Chair this week underlines the enormous opportunity and why I said this in my OB Top 20 post TEK is #3 but arguably could be the top performer. And here we are (again).

Even though it is up 60% YTD, it remains at a 45% discount (assuming ReVive is worthless). In fact, you can buy still buy TEK cheaper than SALT since you pay 11p for 11.78p worth of SALT ownership! (Plus get 4 other holdings for free)

My upside end of 2025 “what’s possible” estimate for TEK of £1.56/share is starting perhaps to not look quite so unrealistic since SALT seems well on its way to get there - and possibly beyond. What happens when all the others start performing like SALT? TEK has outperformed in the past. TEK is in green below.

POW up 22% YTD

Positive update after positive update is taking POW higher as I anticipated it would. But it remains incredibly cheap based on the news flow and accretive value.

So far this month alone:

£1.3m raised at a 3% premium to the share price.

Drilling at Molopo begins - (87% owned) - Targetting Nickel/PGMs

Sampling at Tati - extensive indications of 1g/ton Gold in the over burden even at surface. Next step - what lies beneath?

(Via its FCM holding) Zigzag sampling rare earths and lithium found in commercial quantity and indications of three structures now identified. Drill results for the 1st structure pending.

(Via FCM) North Hemlo drilling along the margin of FCM’s claim returned 1.8% Ni and 1.0% Cu over 1.5 meters

(Via FCM) drilling results show high grade gold assays up to 18.8 g/t gold (Au) / 0.3m channel sample

(Via its GMET holding) Pilot Mountain which in POW-wow potentially contains $1.37bn worth 12.53Mt at 0.27% WO3 less costs with significant copper-silver-zinc credits. This week that same 12.53Mt comprises of approximately 40% Garnet. Garnet sells for up to $220 a tonne. So a further up to $1.1bn (less any further processing costs) on top of the $1.37bn less costs net of credits.

Despite all this news, GMET is slightly less spiky (it’s down) while FCM is less spooky (it’s up) so no net gain. POW is up 10% since all this news but remains substantially discounted. I’ve factored in the £1.3m of cash and the dilution (130m shares) which leaves us 34% discounted on POW direct NAV and the market prices of its holdings, or 48% stripping out cash. Remember 48% based on a NAV (book value) reflecting the value of the land and not the value of the asset under the land!

TMT up 8% YTD

I’m very excited about as its BOLT holding continues to do well and a read across from peers Uber and Lyft bode well if an IPO happens this year. Bolt is now in the UK and growing fast. This was an interesting comparison between Uber and Bolt and crucially Uber take a 25% cut and Bolt take 10%-20%. When the availability of vehicle determines the reliability of the service, one has to wonder whether we will see more and more from Bolt here in the UK?

Meanwhile BLZE is shooting upwards ahead of its Q4 update next week. My fair value tracker shows TMT has an estimated unrealised post period upside of $53.5m (that’s 60% of its current market price!) Or put another way TMT’s holding of Bolt alone on a mark-to-market basis to Lyft and Uber is over $12m higher than its share price! If you strip out my estimate of the value of BLZE and BOLT plus last cash it appears for every TMT share you could get $4.48 a share back out (i.e. $1.42 a share profit) and still hold 55 other holdings worth $137m ($4.42 a share) at last valuation!

Other gains

FAIR (up 3% YTD) and REA’s (up 12% YTD) dividends arrives soon (remember part of the OB20 return will be total return including dividend)

BSRT (up 11% YTD) updated a move in NAV due to FX and CLDN’s share price weakening, but gold remains at $2,036 so am not concerned.

CGEO (up 8.7% YTD) continues to build and build.

PDG (up 8% YTD) completes its divestiture and its rebirth begins….

TRR (up 5.7% YTD) reported a positive Q4 and I’ll be writing about that soon.

Last but not least ANIC (up 5.5% YTD) reported a December y/end NAV of 16.9p a share or a 39.6% discount to the ask price. This week reported important progress at BOND and its strategic agreement with Colgate-Palmolive for supply of precision fermentation animal protein for pet food. I’ll be writing more about that soon too.

Conclusion

Phew! I only meant to write a short note!

So there you have it reader, the bad, the better, the good, and the shoot the lights out. Plenty of anti-OB ammunition for the pessimist; and plenty of OB-positive food for thought for the optimistic.

Make your choice reader. Ammunition and food - just like guns and butter - you choose your point on that continuum.

This is not advice

Oak

I really enjoy your articles and the way you "show your workings" a la DGI9.

The price action prior to the Investigation RNS was bit of a "watch it flag". I think you are right in that the sale will go through and the market has just "knee jerked" and panicking early.

Any views re GROW. Increased insider buying, BlackRock etc... ?