Fright or flight

The Fun Run October 2025 Hallow e'en update

Dear reader

It’s that time again so let’s dust off the cobwebs (groan), who’s got skeletons in their cupbroad (groan) and let’s see how fun runners are faring with their winning (and losing) Stock Investment Ideas during October 2025. From frightful performances to frighteningly good progress the colder, wetter shorter days have brought a few upsets and disappointments. Joy too - for those less fortunate. More on that at the end.

Read on reader, read on!

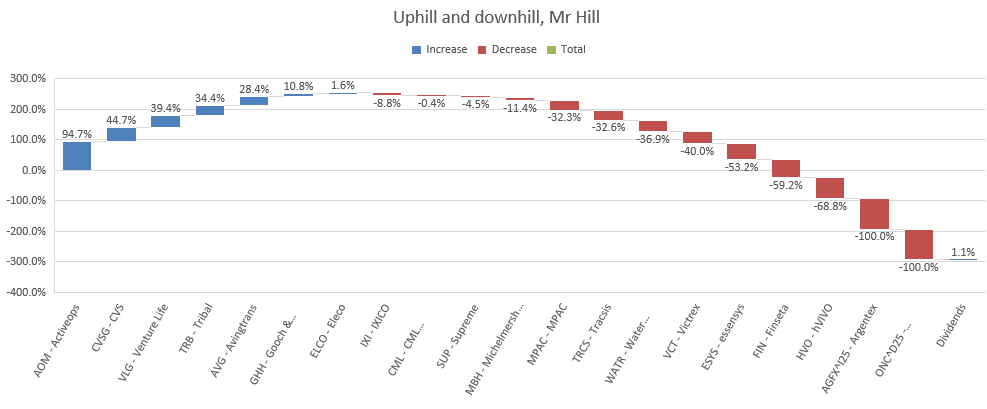

The focus is on spotting trends and opportunities. When things are on a downwards slope for a lagging fun runner, that means the prices of shares they said would do well in 2025 have fallen, but that might also mean overlooked opportunity. The downward slope of Mr Hill’s idea MPAC for example. At 47% off I decided to make that part of my 2026 Fun Run portfolio, even if Stocko label it a sucker let’s see how long until their algorithm changes its mind. It did in 2025. The OB25 for 25 were misfits and suckers, not now. Thanks Mr Hill, if I weren’t glancing left and right to understand the running performance of my peers I’d not have spotted MPAC.

Mr Hill’s top idea ActiveOps at +95% YTD is flying high too at 210p even if Mr Hill believed its fair value was 154p, and at 122p I said I really liked it in “AOM considered”. Stocko claimed in its May update it “often seemed overvalued” and were neutral. I didn’t buy it back in June and (greedily) held back hoping for a further pullback that never came. Would I buy it today? At 52.5X P/E (per Stocko) it’s still a watchlist for me although my eye is drawn to the fact it was 125X P/E back in June. Stocko have changed their tune on its recent 27% revenue growth update and now say “the valuation does arguably make sense - and is even cheap”. Stock claim its PEG (price earnings growth) today is 1.2. At its 52.5 P/E that means 43.75% EPS growth. But Stocko places the current EPS growth at 77%. So Stocko believe its growth will nearly halve but say its valuation makes sense?! Strange when the EPS is 1.57p y/e 31/3/25 and the forecast consensus for y/e 31/3/26 is 2.84p and 31/3/27 4.97p. That’s 81% growth and then 75% growth - based on three broker guesses. But then I look at the past: 2H24 was 1.5p and 1H25 fell -66% to 0.5p and 2H25 doubled to 1p. So the conclusion from that jumble of numbers is the true PEG is more like 0.66 which means 52.5X is forward forecast to fall to 40X in the next year or so.

Of course picking lagging ideas doesn’t always work, or at least patience can be required. Mr Jon’s 4th worst idea TGA - Thungela - that’s not yet warming my tootsies. It’s -39.7% for Mr Jon and 2nd worst for Mr Bloke’s picks for 26 at -8.1%. I warmed to this idea for a couple of reasons. Resilient demand vs declining supply. TGA has been bracing for a “last man standing” approach for years and has 7 coal mines with a cost-competitive profile in SA and Oz. Apart from safety (#1) and driving down its cost of production its next priority is you and me reader. Shareholders. Its track record is superb. My investment thesis is despite “wishing” for net zero to be the reality I cannot dispute the rising number of voices questioning the economics of net zero and particularly base load vs non-base load energy. Russian coal supply is fast declining and other countries are culling supply. So TGA has a continuing role in today and tomorrow’s world - particularly if Natural Gas proves to be less abundant than the world appears to assume.

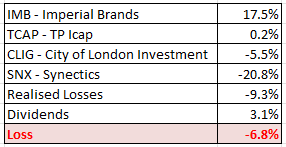

2025 was a bumper year for metals. My top four ideas are Rare Earths, Uranium and Gold. But opportunity lay elsewhere as demonstrated amply by Mr Jon. Secure Trust Bank, Orchard Funding and (OB24 idea) Georgia Capital were all 100%+ for Mr Jon. Fag-flogging Imperial Brands is Mr Head’s best runner is his SIF portfolio and one of our four left in play as at 01/01/25 where it’s the only remaining idea on a real positive at 17.5% (plus about 8.4% dividends). Sharp price rises and continually declining volumes account for its good fortune. Vast buy backs at IMB are underway too.

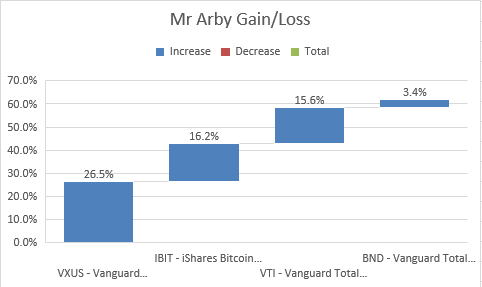

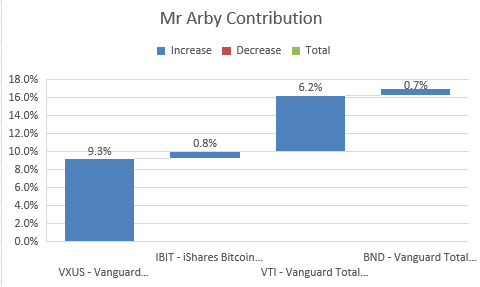

Mr Arby puts some fun-running stockmarket pickers to shame by doing nothing, well 30 seconds isn’t nothing but virtually nothing, and earning 11.7% YTD from four Vanguard funds with VXUS (global ex US) leading the way with +26.5%. Wow. Wow. Wow. That’s two years in a row Mr Arby has outpaced pickers by saying don’t pick. Just buy the index, you’ll be ok. It’s a lesson for everyone that perhaps you are wasting your time reading the Oak Bloke and reading RNSs and company reports. Think what you could be doing instead.

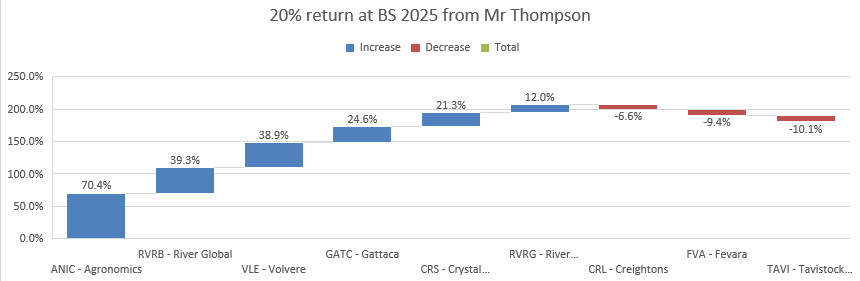

Who have I forgotten? There’s another fun runner. Oh yes. Thompson. The once-vaunted Bargain Shares list where boasts of double digit returns over decades leapt from the pages of the much-read IC. Disappointment reading the IC and the outcomes of some of the ideas Thompson wrote about was a bit of inspiration to start the Oak Bloke. Also realising that half of it was a cut and paste of broker notes. The Fun Run was (apart from a bit of fun) designed to examine the truth of performance - not just some selective truths or conveniently forgotten disappointments. La Verita, nuda e cruda.

BS 2025’ top idea has delivered a 70% return for Thompson. That’s OB 24 idea ANIC - Agronomics. I haven’t written about ANIC for ages and a lot has happened. If I could pick ANIC for the picks for 2026 I would without hesitation. I fundamentally believe that a number of its holdings are on the cusp of transforming our world - as we know it. Pressure on farming continues and the lie of “official” inflation when you go to the supermarket is there on the shelves lightening your pocket. Many products have doubled in price or more over a few years. If we didn’t have digital money we’d be heading towards Weimar-style wheelbarrows.

ANIC is investing in the answer. Technologies that could produce food many times more efficiently than today would be worth trillions. That’s a fact, but the question is will it?

One aspect I’ve noticed during 2025 is a move at ANIC’s holdings more towards ingredients, so rather than growing parts of a cow, so to speak, produce collagen or proteins that go into food. Avoid scaffolds since they are very pricey. Make gloop because egg whites are gloop, collagen is gloop. Start with gloop. Watch out for gloop, and potentially the profits of gloop.

Here are Mr Thompson’s results putting him in 3rd place.

I was quite sceptical about CRL, FVA (was CARR) and TAVI in “examining Bargain Shares Part 1”. So the triple minuses aren’t a surprise to me. I didn’t ever write a Part 2 and Part 3 so would I have been more positive about Mr Thompson’s other ideas? ANIC certainly yes, don’t know for the rest. Perhaps I shall get to them some time.

#4th Place - Mr Arby +17%

Because the split is 35% VXUS, 5% IBIT, 40% VTI, 20% BND the contribution of VXUS is 9.3% (i.e. 35% of 26.5%)

#5 Mr Head down -6.8%

Four ideas remain and 16 have been binned during 2025 at a -9.3% average loss. Often ideas were reported as sold months later so I’ve used the price at the date of the announcement to call time - not the price months before. Sorry but that’s the only fair way to do it.

Mr Head’s dividends which are £616.04 on £20,000 reduces the loss to -6.8%

#6 Mr Hill down -13.6%

Top idea Active Ops up 94.7% ranging down to -100% for Oncimmune & -100% Argentex which both went bust with complete loss of capital. £215.39 of dividends on an imaginary £20,000 where £1000 is invested in each idea at a £4 dealing charge on 01/01/25. Mr Hill called time on Ixico during his weekly broadcast with Mr Scott on 19th June which at the time would have been an -8.8% loss.

His 6th worst idea MPAC became his 9th worst idea, and it joined the ranks of the picks for 26. I’m optimistic about its prospects for 2026 as set out in “MMMPAC”

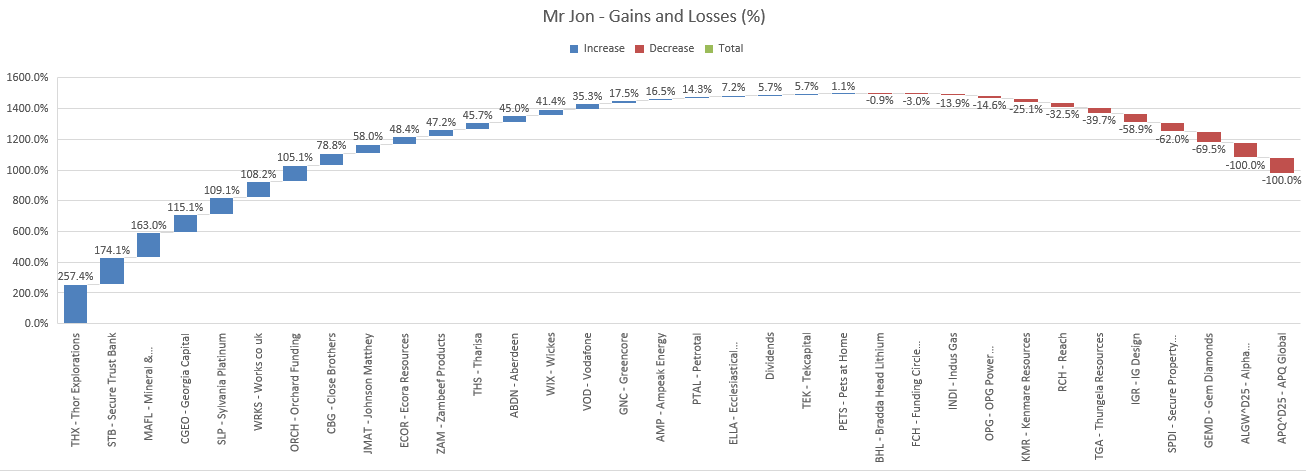

#2 Mr Jon +43.4% performance

Not sure why I’ve gone 3rd-6th then to 2nd place but there we go. Mr Jon holds steady in October with THX a little off its recent highs.

Only 5 of the 25 ideas trade above 10X price earnings (TTM), and 9 of the 25 trade above their book value (P/B). Mr Jon remains an awesome competitor and could easily take the lead again. Of that I’ve no doubt.

PTAL

Some ideas are OB24 like PTAL which recorded a far stronger 3Q25 (production +21%) vs last year. The drought in the Amazon’s dry season appears less severe this year. It has suffered a few set backs in 2025 with faulty tubing and leaks but continues to churn out a 13.1% yield which I greatly enjoy receiving (I hold). It continues to do significant buy backs and despite its high returns it has a cash mountain of over £100m (on a market cap of £327m). It is hard to believe it is as cheap as it is. My instinct is that Mr Jon has more great ideas with a lot further to run and I should spend some time deep diving them.

SPDI

I take a look at SPDI down -69.5% although am beaten back by the complexity of the accounts. Beaten back - not beaten. Looks like if I go through it carefully there could be large amounts of value although relative to a -70% drop I ponder the basis for Mr Jon’s inclusion of this one. At 233% today’s market cap it would seem to be fair value. Perhaps there’s more there. It’s one for another day.

WRKS

a few weeks after I wrote “Quirks” WRKS reported an inline trading update where they are confident in delivering an Adj. EBITDA of £11m and are trading ahead of the market. i.e. the strategy “Elevating the Works” is working.

In my estimation an £11m EBITDA could translate to a £5m net profit which with WRKS at today’s £27m market cap would place WRKS on a 5.5X multiple. It’s down -35% from recent highs, and that seems like a 35% discount for no good reason!

TEK

ex-OB24 idea TEK got to 11p and has dropped again to 9.5p. I called time in “TEKKED OFF” in August at 7.225p with a 16% return but missed this further gain. Quite a number of readers unsubscribed that day. Clearly my decisions and commentary were displeasing and the chattersphere echoed with harrumphing about the clueless Oak Bloke. The Jury is out on that one. Hopefully some readers locked in a gain by selling TEK at the recent 11p high. I do appreciate that there is a possibility of greater gains via the IPO of Guident. I also wonder whether it might be an awful flop. I mean it isn’t as though they have any solid revenue, profit, growth or persuasive content - at least none that has ever been disclosed.

But there is reason to hope. TEK raised £0.37m at 10.5p and zero discount. Its GEN IP holding actually generated cash. Ok it was only $0.24m but it was cash generative. Guident does have its patents. But they’ve not once demonstrated that those patents are reasons that the robotics industry need to knock on Guident’s door to include humans in the loop via Guident’s tech.

Meanwhile TEK has set backs too with ex-OB24 idea BELL that went to -100%. I also called time on BELL in April 2025 admittedly at a dreadful -96.6% loss. I salvaged 3.4% which would have gone to zero. A small positive in a big negative. All my prior articles of sheer positivity about BELL (a view honestly held) remain on Substack so detractors can use those to demonstrate how clueless the Oak Bloke is. And perhaps the Jury isn’t still out after all.

You never get everything right. Mr Jon hasn’t. Mr Bloke hasn’t. Other 2025 Fun Runners certainly haven’t. One of the sensible things Mr Hill once said was aim to get 70% right. Don’t beat yourself up about the 30% you get wrong. That lesson stays with me and guides my instinct when I hover over the buy or sell button. Always buy for a reason. Always sell for a reason. What’s the reason? Don’t know? Then DO NOT PUSH THAT BUTTON.

Is investing really just that simple?

2024 Fun Run

I still haven’t properly gone back over the discrepancy with Mr Scott’s but the results excluding that at +22 months are:

Mr K Roast 40%, Mr Archer 36%, Mr Arby 22.2%, Mr Bloke 7%, Mr Scott 0%, Mr P Roast -60%.

Mr Roast’s three ideas were Guardian Metals at +247% while East Star is at -54% and TM1 at -74.4%. Guardian, like OB25 for 25 idea Mkango and Energy Fuels (UUUU) are beneficiaries of Trump’s State interventionalism. Mr Archer included GMET 6 months earlier so is 988% while Asia Met is now +32.8% with Sovereign at -7.8% and another 9 ideas ranging down to -100% for HellenicDynamics.

The “2nd lap” race leaders have much to thank Donald Trump for, although arguably Guardian has always a superb share and ably led by Mr Friesen.

POW

The OB 2024 idea POW benefitted from GMET ascendancy although only in terms of cash proceeds (Tranche #1 sold for £9.2m, Tranche #2 sold for £13.6m = £22.8m) and not the share price performance. POW at £15m market cap (!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!) remains -19.7% and is one of the most mispriced shares in the UK - in my opinion.

Between its stake in:

1. £4.2m for 30% of Fermi and its £10m Uranium exploration programme.

£1m for 35% of Blockchain-based Minestarters, for decentralised trading of early stage miners with rules-based disclosures, rewards and performance. Rules and disclosures improve the friction of mistrust and fat commissions taken by Brokers and Intermediaries, and will help investors exposing liars standing at the top of holes in the ground, while money can pour into progressive companies like Guardian who via Blockchain disclosures and a “chain of custody” of evidence can direct productive capital into the ongoing need for metals and minerals.

A £4m 16.66% stake in Apex Royalties the de facto UK successor to the delisted OB idea Trident (TRR)

75% of Chemical Engineering and Metals Recovery GSAe

A ~10% stake in FCM worth £0.4m and a small stake in Australian listed AAJ.

An 82.3% stake in Power Arabia and its highly prospective copper project

A 43.44% stake in newly-listed FDR (£3.1m marcap) Gold prospecting on the doorstep of Billion Pound Greatland Gold.

A 25% free carry on the development of Gold prospect Tati (with 100% ownership)

A 87.7% in Molopo a PGM-Nickel project.

Plus an estimated £10m remaining cash after the above, so all the above you can buy for a net £5m if you strip out the cash - POW might engage in buy backs.

Can you see why I added so many exclamation marks for POW?

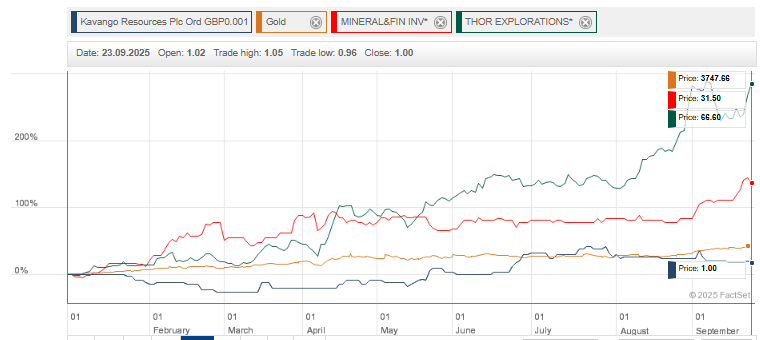

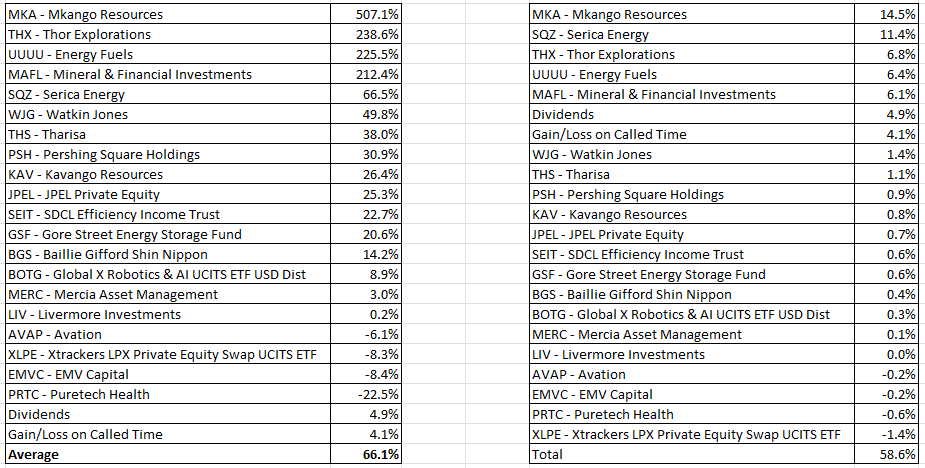

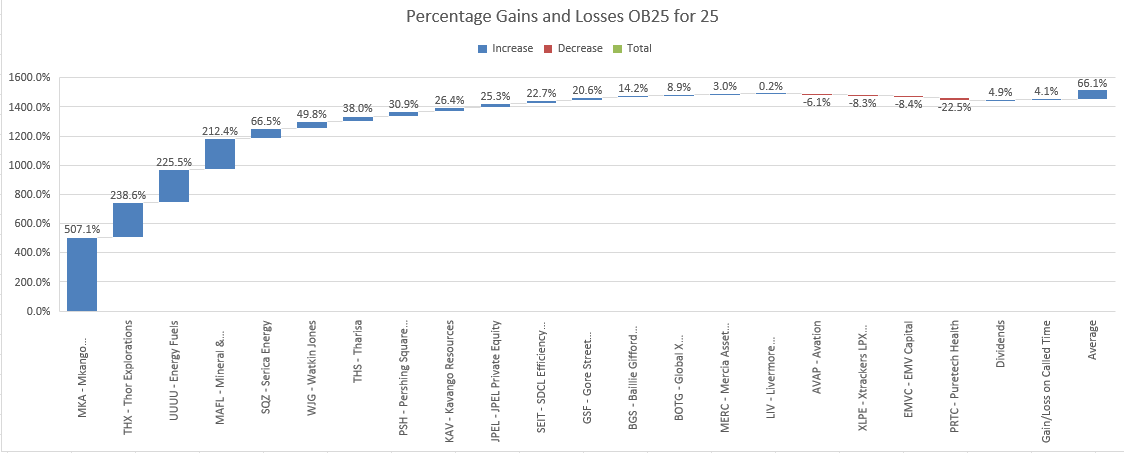

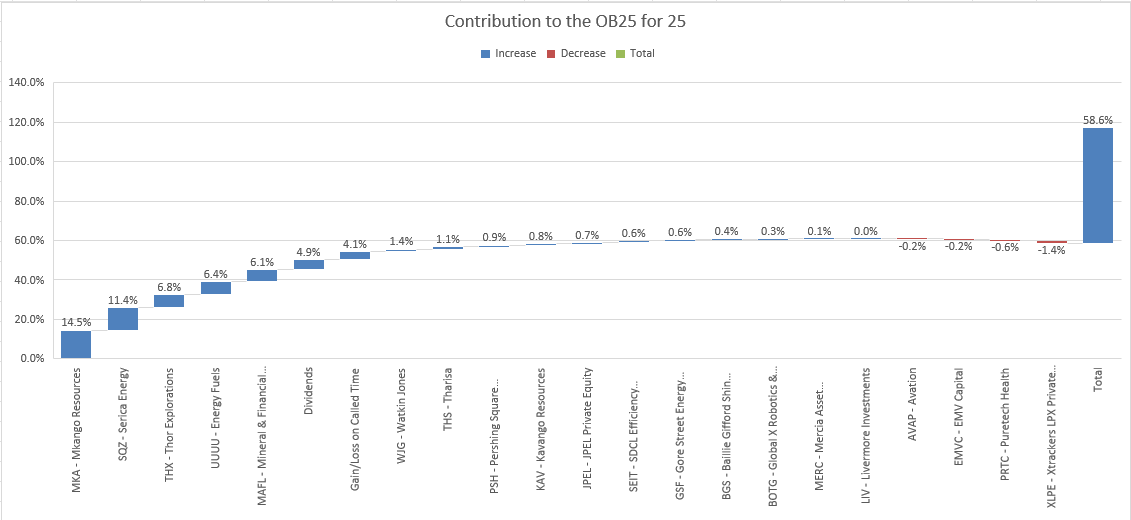

#1 Mr Bloke OB25 for 25 +58.6%

Is a 58.6% return unassailable? Hardly. The recent pullback in Gold cost me -3.4% (from +62% to 58.6%). Can further declines hurt me? Can rusty Triton the FPSO ship creaking in the North Sea swells and go Oooooo! once more in 2025?! Of course it can.

Let’s briefly cover as many of these as possible.

Let’s go from the worst to the best:

#1 PRTC -22.5%

Biotech Puretech is down -22.5%. Given the ongoing rerate of Biotech I’m pretty relaxed that even in the next 2 months PRTC is going to reawaken. I spoke at some length on the reasons why in “PRTC doesn’t make”. So much length that (to my supreme satisfaction) it irritated Grezzz.

Sadly no one answered Grezzz’s question, until now. This one’s for you Grezzz.

Oh, Grezzz, thou dost cast a shadow upon The Oak Bloke’s verdant verbosity, deeming my pun-laden prose a thorny trial! Yet, let me weave a tapestry of flowery retort: my quill, dipped in the ink of wit, sprouts puns that blossom with mirth, making the arduous trek through my tomes of articles a delightful gambol through a lexical grove where you may graze Grezzz.

As for my prognostic prowess, fear not. My probing unearths winners with a regularity that rivals the best, though I cloak my words in petals of playful rhetoric, where every pun is a bud bursting with insight - as you says Grezzz!

(Do thy own research and thou makest thine own investment decisions, innit)

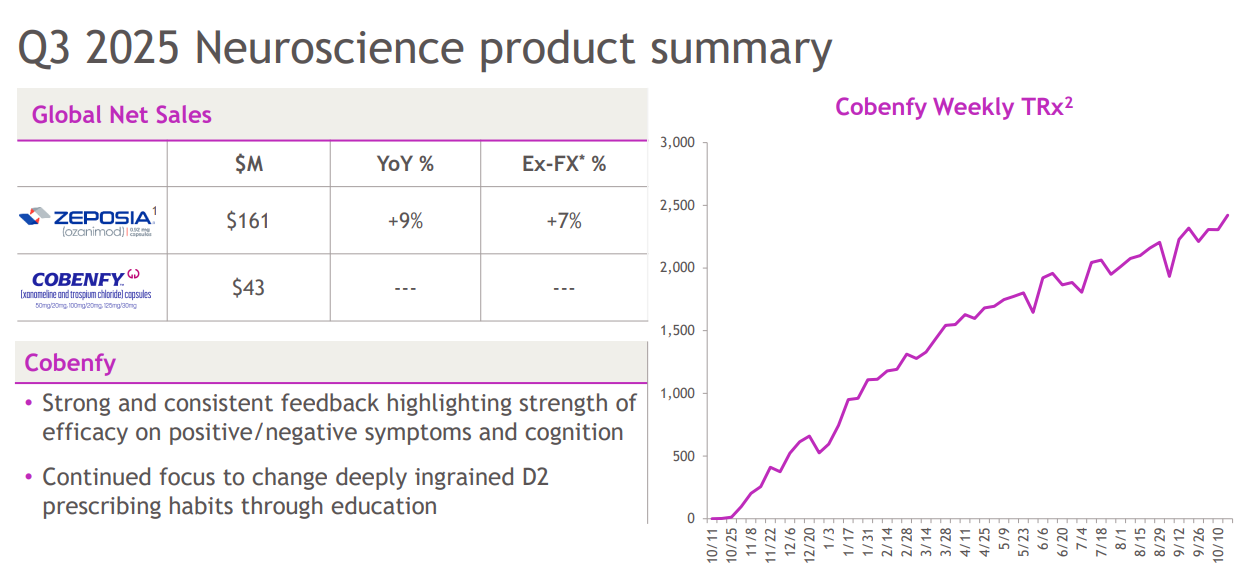

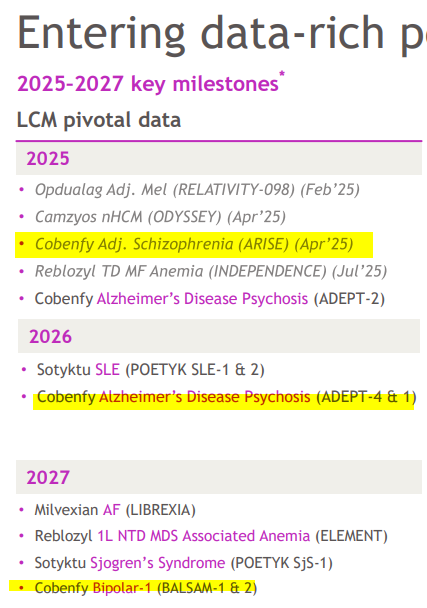

To prove the point that PRTC is undervalued relative to its subsector consider this chart.

Sales of Cobenfy continue to grow for BMS. That’s its Schizophrenia drug which it bought from PRTC and which shall attract both milestone payments and hopefully royalties for PRTC as it continues to grow. Q1-Q3 they grew: $27m → $35m → $43m

Bristol Myers Squibb have several angles for Cobenfy’s expansion.

#2 EMVC -8.4%

The move up of Health Tech, such as the success of IP Group’s Hinge Health is hearty news for EMV Capital. Not news that has yet fed to EMVC’s share price. This time next year Rodney. The green tech within EMVC feeding on Labour government spending is another beneficiary too.

The rapid rises in other VC such as at GROW and CHRY are encouraging too.

#3 XLPE -8.3%

XLPE is down -8.3% and because I leaned in on that 6X then that’s equivalent to another holding being down -49.8%. Ouch! With a growing flow of IPOs in the US and elsewhere even green shoots in the UK. Deal flow has slowed down though through tariff uncertainty, and that’s limiting liquidity. PE doesn’t only rely on deal flow and asset management income remains robust. In fact XLPE holdings are starting to report their 3Q25 earnings. What are they reporting? 100% report at or above estimate earnings.

#1 Blackstone $1.9bn earnings - beats estimates, #9 Ameriprise EPS $8.81 (beat) driven by asset mgt fees growth, #16 Main St Capital EPS $1.25 (in line), #17 New Mountain EPS $0.37 (beat), #20 Hercules EPS $0.49 (beat).

#4 AVAP -6.1%

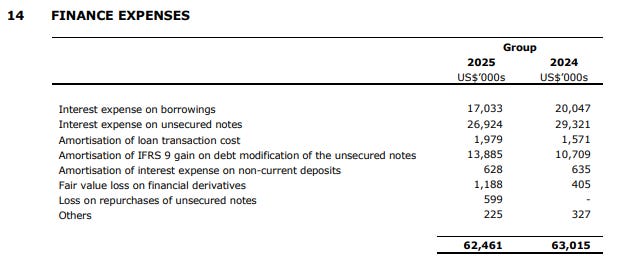

Despite a strong FY25 covered in “AVAP-orising” and now certainty around debt financing albeit at a higher rate than I had anticipated (8.25% vs 6%)

Although 8.25% is $24.75m per annum vs $45.5m in FY25 (plus the $17m Interest expense on borrowings - which remains albeit will move lower in FY26 perhaps by ~$3m).

So my forecast of a ~$20m cash flow (and profit) benefit appears to remain the case. We are not told of other costs like arrangement fees, but perhaps there were some.

#5 LIV 0.2%

A fair value loss on CLOs during a bumpy 1H25 netted off against investment income to deliver an overall small loss.

But the market is comatose asleep to the 350% post period upround at Fetcherr announced some weeks ago - a great example of the application of AI into something incredibly profitable. Pricing for Airlines.

I covered LIV earlier this year in “Peachy”. LIV holding in Fetcherr was worth £11.1m at 30/06/25 so appears to have been revalued by +£27.5m to £38.6m post period

But the whole of LIV is a £81m market cap! That +£27.5m is a ~35% uplift nowhere in the price!

Fetcherr’s pipeline is growing faster than they can keep pace.

#6 MERC +3%

Rather than a flashy ride, steady Eddie MERC has been keeping it quiet. Purring along quietly.

A recent T/U at the AGM said it had had a positive start to current financial year. That it is “Well-positioned.” Cash levels are at £35m. A £3m buyback is ongoing.

In “Merc gives a smirk” I recognised £3m of hidden value. Will more be revealed in a months time when they released their results to 30th September. I’m looking forward to that.

#7 BOTG +9%

NVidia is now a $5tn market cap and is the largest component at BOTG. Considering that 12 months ago no one was speaking about Robotics, during 2025 many have begun to speak - including Mr Mellon the man with the telly on - and others like that guy who talks about Factoids.

#8 Baillie Giff Japan Smaller Companies Fund +14%

Considering that the top 10 rose 40% and I’ve covered this most months, 14% is actually quite disappointing. They culled the Fund Manager and Mr Lum is supposedly reducing the focusing the fund. Focus Mr Lum, come on chop chop.

#9 GSF - Gore St +20.6%

A hesitant shareholder after owning GSF for four years, called Arrrr Ummm Infrastructure decided finally to shake things up. The BOD are being replaced with skilled, experienced and independent indivuals - they say.

A focus on the single grid of Great Britain is apparently the new focus. Germany will be sold off. Pre-Construction assets (of 495MW) sold or developed via partnerships. 130MW of augmentation to two hours will occur during 2026. Assets in the USA, and the island of Ireland are under watch.

Meanwhile GSF’s trading outperforms the 1-hour benchmark prices by a wide margin and NAV holds steady at 102.8p implying a near -40% discount still.

#10 SEIT +22.7%

SEIT grinds higher but remains on a substantial discount. Its 1H26 results to 30th September are a month away. The preceding trading update suggests an in line performance with some disappointments while some holdings make strong progress.

#11 JPEL +25%

Another beneficiary of Trump’s Big Beautiful Bill Act is JPEL whose largest holding (60.3% of NAV) is an R&D tax advisory. Full expensing of R&D against Tax means a bumper crop of new business and therefore there is “confidence” in a valuation upside. The share has reacted modestly to this news up 10% although JPEL remains on a 26% discount pre-valuation upside.

#12 KAV +26.4%

Kavango proudly flies its unlucky “sucker” epithet and is an idea that not yet blossomed still, 10 months later despite a 50 tonnes per day operation being under construction, with plans for a 200-300 TPD extension in 1H26, and has revealed highly attractive sample levels of gold in its updates. No JORC resource has yet been defined. It has a cash war chest of around US$10m.

In surprising news CEO Ben Turney was thanked for his contribution and left with immediate effect. I would add a huge thank you to Mr Turney from myself and Kavango shareholders - he will be missed.

Mr Wynter Bee is stepping in and has hastily assured investors of the new board’s experience working together in Reunion Mining Plc (spot the irony) in Zimbabwe asset which was then sold to Anglo American Plc. Can history repeat itself?

KAV has not substantially increased with the gold price in 2025 so remains an elusive and undervalued share where sudden newsflow could launch this skyward. The potential of its assets is exciting, and with substantial funds raised

It’s down 20% on the news of Mr Turney’s depature since this chart was published in September.

#13 PSH up 30.9%

Canny Mr Ackman has played some blinders this year geting NAV to £65.64 from £56.81. Fannie Mae and Freddie Mac remain a potential beneficiary of Trump deleveraging the US balance sheet. Turnarounds at shares like Nike continue although Chipotle has proven a disappointment in 2025.

#14 Tharisa up 38%

With PGMs remaining in deficit it’s true this has followed gold but is also enjoying higher basket prices based on fundamentals of demand and supply too.

THS reported 4Q25 to 30/09/25 at +19.7% PGM production to 41.3Koz beating guidance by 5Koz, while Chrome at 1.56 Mt is a slight miss of 10 Kt. THS had some challenges with rain and flooding in 2025.

Chrome pricing was slightly above lower guidance at $266 vs $265 per tonne but PGMs was above the upper end of guidance at $1615 vs $1600. The 4Q25 basket was $1953 per ounce!

My outlook is even at its higher £288m market cap this is below a forward P/E of 3X, although that is a back of a fag packet calculation - and close to 2X…. a full article will more closely consider this. Today in 1Q26 the basket is now well above $2,000 an ounce.

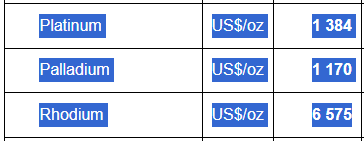

‒ The PGM market and in particular platinum has been one of the strongest commodity price performers in 2025, with the continued deficits, constrained supply, and tightening stocks acting as strong tailwinds. Palladium, however, faces a more delicate balance, while the minor metals have seen good price support driven by healthy supply demand fundamentals, which should see continued support for current prices

NB: Platinum is historically 56.2% of the Tharisa Mine basket, with 9.5% Rhodium. In 4Q25 it was 54.7% Pt and 10.9% Rh

Platinum is +$200 an ounce vs 4Q25 and Rhodium is +$1645 an ounce.

#15 Watkin Jones - up 50%

A net net with cash equal to its market cap and 40% below NAV the question is whether delays will unjam. Its FY25 trading update was inline. This one needs an article and closer examination.

#16 SQZ 66.5% (at a 6X weighting)

Serica with an imaginary £6k invested (instead of £1k) is magnified to give a 399% gain. In September I wrote “SQZ-ing has its risks” but declared this a rugged fighter and quality management.

Since then that has been demonstrated in a deal with BP for its North Sea assets, where BP want to get the heck out of B and produce P in other countries than B.

I got a bit of stick from some people about Serica, but despite its various setbacks its got up again and fought on and performed exceptionally well considering. Triton is finally operational at 25kboepd. Hurrah!

I am very excited about its forward prospects in the final months of 2025 and beyond. It remains a medium to long-term idea where it’s a well-run business with interesting and vital assets which are going through challenges and shall emerge stronger. Where SQZ can hoover up further assets cheaply as many companies defocus from the North Sea. Unloved assets have the advantage of price.

#17 MAFL +212%,

#18 UUUU +225%,

#19 THX +239%

and #20 MKA +507%

These deserve an article in their own right so will circle back on these. I note questions from readers about these and the quick version is I remain excited in their forward prospects.

Their performance and particularly their speed of performance have exceeded my wildest expectations. I put a lot of work into researching and selecting them, and while my selection of picks for 2026 I have set myself a high bar.

#21 - #25 NBDG, KDNC, OCN, WATR, APAX - called time.

FINALLY - Joy

I don’t rattle the tin often but I shall again today.

The days grow colder and somewhere in your heart can you be warmed - if you’ve not contributed - but have been reading and enjoying (except Grezzz) the 265 articles I’ve so far written in 2025 “on your marks” was article #1 of 2025 in case you’re wondering - you know it’s the right thing to do.

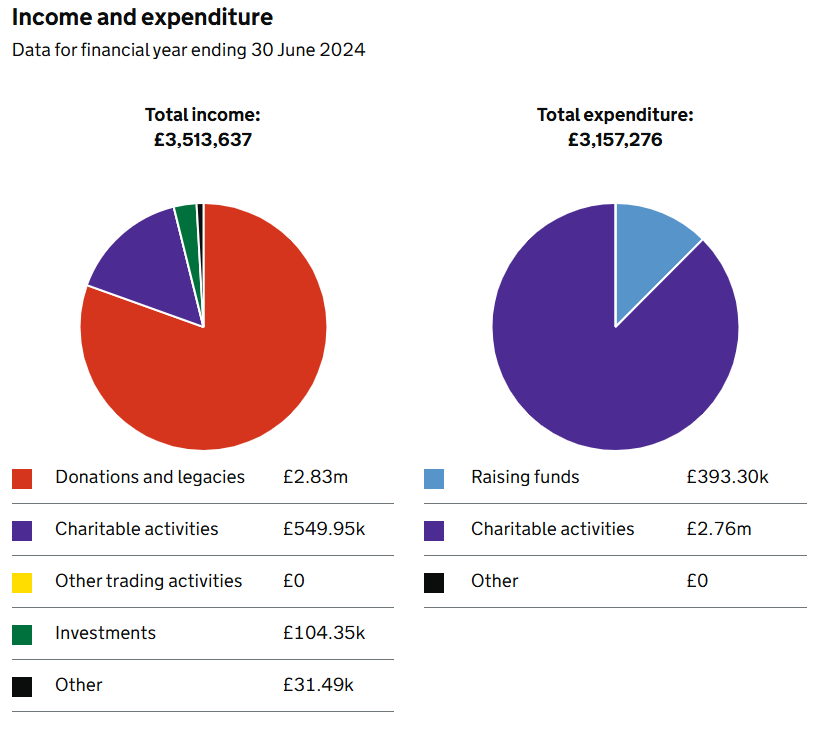

Look at the article views below. There are THOUSANDS of people who silently skip this bit. Don’t be one of them I urge you. Be among the 140 PEOPLE who have contributed to Emmaus as a recognition that there are less fortunate people and we can give them a HAND UP NOT A HAND OUT this November. In advance, thank you.

Donate here

Emmaus isn’t a large charity so we can make a real difference.

Terry Waite is the President of Emmaus and has tirelessly worked to drive change since his release from 5 years of torture, mock executions and solitary confinement in 1991 from those not so lovely people in Lebanon, Hezbollah.

Oak Bloke readers have contributed the equivalent of 0.2% of Emmaus total annual income (based on 2024). How amazing is that?

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

I find I can’t agree with Grezz, so keep the purple prose coming, alongside your sharp insights. Donated.

There’s a nice Buffettism about not having to get everything right

“It’s how much you make when you are right, and how much you lose when you are wrong, that counts”